Our strength: remote banking introduction*

Responsiveness in real time on our chat online, in English or French, our permanent follow-up and our assistance included in all our packages.

The Premium Pack includes :

- LLP company formation in London (UK), with no need to travel, banking introduction* HSBC.

- Whatever your nationality, you can set up your company in London in 1 day, 100% online. You don’t need a London address, you don’t need to be resident in London, and you don’t need a visa. Share capital from £1.

- Ultra-fast bank introduction* assistance*.

- Bonus (free): 3 exclusive business ideas not yet exploited.

- We guarantee comprehensive, high-quality services, with complete transparency and a climate of trust; we guarantee real-time availability 6 days a week, 10 hours a day, follow-up and assistance… Find out what our customers have to say about us.

- Boost your business with our Europe-wide network of contacts (manufacturers, distributors, suppliers, resellers, local agents, logistics and goods-in, etc.).

Don’t leave your company incorporation to just anyone. With us, you benefit from the following advantages and guarantees:

- Unique, take no risk: company incorporation and registration guaranteed satisfied or reimbursed.

- Possibility of undeposited share capital, starting at €1

- We take care of everything

- Ultra-fast bank introduction* assistance*.

- Immediate reactivity

- Company incorporation in 1 to 2 working days

- 100% online (no paperwork), no travel

- Payment in 2 instalments

- We speak English

There’s no need to travel to set up your company, or to introduce your bank*. What’s more, we speak French.

The Premium Pack: SOCIETE LLP 100% online, no need to travel | Pay in 1 or 2 instalments | banking introduction* included

Pay in 1 instalment € 990 + VAT

Pay in 2 instalments, deposit €524 + VAT

Great promo :

LLP + HSBC banking introduction*: 1490 € + VAT or in 2 instalments 756 € + VAT. Possibility of payment by bank transfer

Show that your company has a long history:

LLP company ready for use (already registered) :

LLP 2023 + HSBC banking introduction*: 1990 € ht or in 2 instalments 1015 € ht. Possibility of payment by bank transfer

- When you place your order, you will automatically receive an e-mail with a Company incorporation form to fill in.

- Payment can also be made by bank transfer: you can place your order above: during payment, you will be offered the option of paying by bank transfer; click on the “Bank transfer” box: when we receive your order, we will send you our bank details for your transfer, with the option of paying in 1 or 2 instalments.

![]() [email protected] (in english or french)

[email protected] (in english or french)

![]() +33667896739 (in french)

+33667896739 (in french) ![]() whatsapp (in french)

whatsapp (in french)

- Would you like to be reassured about our services? No problem, we can provide you with the telephone numbers of one or more of our customers.

Banking introduction* (online banking, CB,...) to Revolut Business, Wise,... : €0 (included in all Companies incorporation orders)

OR

Assistance in English (an independent account manager, employed by the bank, calls you and takes care of your request to open an account with Revolut Business or with one of our other partners) : €290 + VAT.

OR

Banking introduction* in a real bank in Europe (French language), network of banking agencies in a country bordering France, with travel : €392 + VAT.

OR

Banking introduction* in a real bank, with a network of branches, WITHOUT TRAVEL (which is rare for a real bank), with of course online access, remotely and with an independent account manager, working for the bank, english and french : without travel, €392 + VAT.

OR

HSBC banking introduction* in a European Union country: €890 + VAT.

You can, of course, opt for an online banking introduction* (neo-banking: Revolut Business or another of our partners), which is included free of charge in all our Company incorporation packages.

Among our strengths :

- Fast, guaranteed company registration in around 1-2 working days (London) + free banking introduction*.

- When you order, we will send you by e.mail, a company incorporation form online to complete and you will attach a copy of your passport or identity card and proof of address.

- Ultra-fast online service (no paperwork and no travel (for certain countries including England, Scotland, Ireland, Bulgaria, Malta, etc..

- As soon as your company is registered, we’ll e-mail you the PDF incorporation documents. You’ll receive your company’s documents by e-mail in real time.

- Free customer support in French, 6 days a week, from 9am to 7pm.

New: contact one of our customer advisors. Would you like to be reassured about our company? We can put you in touch with one of our customer advisors on request.

LLP

A Limited Liability Partnership (LLP) is an alternative type of company structure that is popular with professionals who often operate as partnerships, such as lawyers, doctors and architects, but whose members require limited liability. Other professional activities can be managed by an LLP, and are of course not restricted to the liberal professions: services to professionals and private individuals, consulting, auditing, engineering, intermediation, brokerage, advice, matchmaking, management, training, communication, intermediation between suppliers and buyers, management of private funds or portfolios, holding companies, etc.

An LLP has no directors or shareholders; instead, there are members, more commonly known as “partners”. There must be at least 2 members to register an LLP, but there is no limit to the number of members permitted.

LLPs are governed by the Limited Liability Partnership Act 2000 and the Limited Liability Partnerships (Application of Companies Act 2006) Regulations 2009, rather than the Companies Act 2006.

Hague Convention – 1992 – Decree 92-521 “Any natural or legal person resident in the European Community has the right to set up a company in the country of his choice without having to be resident there for tax purposes”.

The LLP method of taxation provides a greater level of tax transparency, as well as allowing members to remain separate.

You can designate another company (called a “legal entity”) to be a member of an LLP.

LLP members can be based anywhere in the world – they need not be resident in the UK.

LLPs, whose sales are not made in the UK and whose members are non-residents, are not subject to corporation tax; only the members are taxed in their country of tax residence*.

{kind=link}

{kind=link}

What is a Flow-Through (Pass-Through) Entity?

A pass-through entity is a legal business entity that passes on all the income it generates directly to its owners, shareholders or investors. As a result, only these individuals – and not the entity itself – are taxed on their income. Pass-through entities are a commonly used means of avoiding the double taxation produced with conventional corporate profits and the income of owners, shareholders or investors(1).

Professionals who use LLPs tend to rely heavily on their reputation. Most LLPs are set up and managed by a group of professionals with a wealth of experience and clients. By pooling their resources, partners reduce operating costs while increasing their LLP’s capacity for growth. They can share offices, employees and so on. More importantly, reduced costs enable partners to realize more benefits from their activities than they could individually.

Another advantage of an LLP is the ability to attract partners and let them go. Since a partnership agreement exists in an LLP, partners (members) can be added or removed as specified in the agreement. This is convenient, as the LLP can always add partners who bring with them existing business. Usually, the decision to add requires the approval of all existing partners(2).

Form an LLP :

We offer a package and services dedicated to the creation of Companies incorporation of the LLP type.

Here are the key points to bear in mind when setting up an LLP:

– an LLP must have a minimum of 2 members (although you will of course remain the sole de facto owner of the company);

– you must provide information (passport or identity card) on the persons with significant control (PSC) in the LLP; generally, the members are all PSCs, although they have limited liability and are not responsible to each other in any way;

– LLPs must be formed for the purpose of making a profit – this corporate structure is not suitable for not-for-profit organizations.

FAQ :

What is an LLP member?

An LLP member is a partner in an LLP limited liability partnership. You must have a minimum of 2 members to create an LLP.

Who can be an LLP member?

An LLP member can be any person of any nationality, or a legal entity.

What’s the difference between a member and a LLP member?

Members have exactly the same rights and duties as all other LLP members, but they have the additional responsibility of ensuring that the LLP and its members comply with all statutory requirements and obligations. They must ensure that the confirmation statement and annual accounts are filed accurately and on time. They also see to all formalities in the event of the LLP’s dissolution.

LLP members must pay tax in their country of tax residence*.

KEY POINTS

Liability Limited Partnerships (LLPs) offer a partnership structure in which each partner’s liability is limited to the amount he or she invests in the business. Having partners in an LLP means benefiting from the individual skills and expertise of each member, and establishing a division of labor.

Limited liability means that if the partnership fails, creditors cannot come after a partner’s personal assets or income, provided of course there is no mismanagement or other fault.

LLP companies are common in professional businesses such as law firms, accountancy firms, medical practices and asset managers, but their flexibility means that they can also be used for other professional activities, the sale of services (consulting, maintenance, expertise, transport, etc.), advice, intermediation, brokerage, property management, patents and trademarks, etc.(2)

Setting up a foreign company also means establishing an economic substance (actual local organization of the activity: offices, premises, activity, materialization, resources, etc.), which will be complicated for you to achieve in a distant country, in your capacity as owner of the company, if you are not resident in the country where your company is located. The non-existence of economic substance in a foreign company is tantamount to the de facto operation and tax establishment of the company in the owner’s country of tax residence. For a European national, setting up a Company incorporation in Europe means making it easier to establish the company, and then mastering the administrative management, accounting, production, marketing and tax declarations in the country where the company is headquartered. Not to mention the company owner’s tax obligations in his or her country of tax residence.

In France, the LLP can be likened to the SNC: “By default, the SNC is not taxed at company level. However, each partner must declare his or her share of profits and remuneration as industrial and commercial profits (BIC) or non-commercial profits (BNC) on his or her income tax return”. Source : https://www.economie.gouv.fr/entreprises/societe-en-nom-collectif-snc#:~:text=collectif%20(SNC)%20%3F-,R%C3%A9gime%20fiscal,dans%20sa%20d%C3%A9claration%20de%20revenus.

The limited partnership is also close to the LLP legal type. Whether LLP, LP or SNC, legal, tax and other differences apply*.

“The general partnership (SNC) must have a commercial activity. Liberal or civil activities cannot be carried out in an SNC. The SNC is a partnership in which the partners are all merchants and are indefinitely and jointly and severally liable for all the company’s debts.”

Source : https://www.economie.gouv.fr/entreprises/societe-en-nom-collectif-snc

Liability Limited Partnership (LLP): similarities or equivalents: partnerships, limited partnerships, SNCs (non-exhaustive list).

It should be noted that you will need to organize the economic substance of your foreign company, subjecting you to the tax requirements of the place where your company is headquartered and those of the country where you are resident for tax purposes.

LLP VS LTD

Brief comparison of Limited Liability Partnerships “LLP” and Private Limited Companies “LTD” as legal structures in the UK.

LLPs are often used for professional service businesses, while LTD companies tend to be used for commercial enterprises, but there are a number of commercial and tax points to consider when deciding which structure is best suited to a business.

- Similarities

- Differences

- Best option?

1 – Similarities between LLPs and LTDs

An LLP is a hybrid of a limited liability company and a traditional partnership. It aims to combine the limited liability enjoyed by the partners of an LTD with the advantages of flexibility and tax transparency provided by a partnership. LLPs are much more like limited liability companies than traditional partnerships.

As such, Limited companies and LLPs share several essential characteristics, as follows :

- Constitution and set-up

Both LLPs and LTDs are incorporated in England. An LTD company will have directors and shareholders, while an LLP will have members only. The constitutive document of an LTD company is its articles of association (and any corresponding shareholders’ agreement). The equivalent for an LLP is the members’ agreement.

- Legal personality

An LLP or LTD is a legal entity with legal personality, which means that it can enter into contracts, own property and sue in its own name.

- Limited liability

Unlike a traditional partnership, members of an LLP or shareholders of an LTD have limited liability, which generally means that they do not need to meet the LLP’s or LTD’s obligations. The liability of a partner in an LTD company will be capped at the unpaid amount of the shares he or she holds. The liability of a member of an LLP is limited to the amount of capital he has agreed to contribute under the members’ agreement.

Members of an LLP and directors of an LTD company will generally only become personally liable for debts or obligations in certain limited circumstances (such as unlawful or fraudulent transactions).

- Submission requirements

LLP and Limited (LTD) companies are required to file annual accounts with the English Registrar of Companies. Both must also create and maintain a register of persons exercising significant control.

- Fixed or floating fees

LLP and LTD companies may pledge fixed and floating charges against their assets.

2 – Differences between LLP and LTD

Despite the similarities between these two types of company, there are a number of key differences that need to be taken into account when considering the most appropriate structure for your business:

- Organizational flexibility

Both an LTD and an LLP offer flexibility in terms of structure, but the members of an LLP arguably enjoy greater organizational flexibility and are free to agree amongst themselves the affairs and governance of the company. The affairs of an LTD limited company must be managed within the confines of the Companies Act 2006, which imposes stricter restrictions on Limited companies than LLP legislation.

As a result, members of an LLP have greater flexibility in how they share profits, organize capital, their management structure, how decisions are made, how members are appointed and how they retire.

- Confidentiality

Unlike an LTD company, whose articles of association are publicly available from the English Registry, an LLP members’ agreement is private. This members’ agreement covers issues such as profit and loss sharing, capital shares, management responsibilities, admission of new members, retirement, expulsion of members and dispute resolution. If members are unable to resolve these issues, LLP legislation contains certain default provisions, although the best practice is to put an agreement in place.

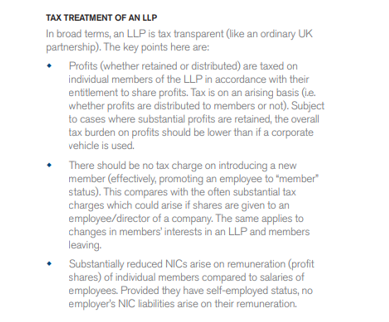

- Tax treatment

For tax purposes, an LLP is treated as a partnership. This means that it is tax transparent, in that the LLP entity itself is not taxable, but the members are taxable as individuals, both on profits made by the LLP and on gains on the sale of LLP assets. Normally, LLP members are treated as self-employed and will be liable for income tax on their share of LLP profits. In the case of an LLP owned by foreigners (non-UK tax residents), the taxation of the members’ countries of tax residence applies. This taxation will be Income Tax and or Non-Commercial Profits Tax and or possibly any other taxes specific to the said countries of tax residence.

On the other hand, a Limited Company (LTD) is considered a separate entity for tax purposes and will pay Corporation Tax on the company’s profits. Shareholders will generally be liable for income tax on their salaries. Shareholders of an LTD company will also pay tax on any dividends they receive, and on any gains realized on the transfer of their shares in the company.

In the case of an LTD owned by foreigners (non-UK tax residents), the tax laws of the shareholders’ countries of tax residence apply. This includes income tax, dividends, gains realized on the transfer of shares in the company, and any other taxes specific to the country of residence. If the foreign company has no economic substance (premises, offices, employees, office automation, actual activities, etc.), the company will be deemed to exist, materially, administratively and legally, by default, only in the country of tax residence of the shareholder(s), with all the tax consequences that this implies.

Investing and selling

LTD companies are often considered more attractive from an investor’s point of view, as they can buy shares in a Limited LTD company, without having to become a director. An investor in an LLP must become a member, and a share or part of an LLP cannot be sold in the same way as shares in an LTD company.

- Share capital

Unlike an LTD company, an LLP has no share capital.

3 – Best option?

LLPs and LTDs are well-known and commonly used types of company in the UK, offering flexibility and limited liability. When comparing them, it’s important to consider which is most appropriate for the business to be set up, as well as the structure required and the nature of its activity.

Find out more about Limited liability partnerships (LLP)

A legal entity with a legal personality distinct from that of its members.

Limited Liability Partnerships Act 2000 (LLPA 2000).

Changes in the composition of an LLP do not affect its existence.

LLPs combine the flexible structure of a partnership with the advantages of limited liability for its members. An LLP owns the company’s assets and is liable for its own debts; members act as agents and are only liable up to the amount they have paid into the LLP. An LLP is fiscally transparent, so its members are generally subject to the same tax treatment as general partnerships and their partners.

https://uk.practicallaw.thomsonreuters.com/Glossary/UKPracticalLaw/Iacc21b1e1c9a11e38578f7ccc38dcbee?transitionType=Default&contextData=%28sc.Default%29

A limited liability partnership (LLP) is a legal entity for company law purposes, but is generally taxed as if it were a partnership (i.e., it is fiscally transparent). This means that when an LLP carries on a trade, profession or business with a view to making a profit, its profits and gains will normally be taxed in the hands of its members, rather than being taxed on the LLP itself. Tax transparency also means that members will be taxed on the LLP’s profits and gains as they arise, whether or not they have been distributed to members.

https://www.lexisnexis.co.uk/legal/guidance/taxation-of-uk-llps

Requirement for LLP members to be self-employed

Individual members

There are no tax obligations at LLP level. Profits are taxed on the individual members of an LLP, in accordance with and in proportion to their profit-sharing rights. https://www.macfarlanes.com/media/1723/structuring-a-business-as-a-limited-liability-partnership_july-14.pdf

Partnerships, including LLP limited liability partnerships, are tax-transparent. This means that the partnership itself is not subject to tax: any profits are taxed on the partners.

As a general rule, for tax purposes, each partner is considered to receive his or her share of the partnership’s income and expenses as they arise. This treatment is overridden in special cases by anti-avoidance legislation designed to prevent partnership structures from being used to avoid (or reduce) tax. The description below focuses on two such provisions: the rules for reallocating profits in “mixed partner” partnerships, and the “salaried partner” rules that apply to limited liability companies.

Mixed partnerships

A mixed partnership is a company that includes both individuals and non-individuals (most often, but not necessarily, companies, and hereinafter referred to as “associated companies”) as partners. Since April 6, 2014, partnership tax anti-avoidance rules have applied to mixed partnerships whose profits are transferred from individual partners to corporate partners in order to reduce the overall tax liability. These rules apply to both partnerships and LLPs.

The intention of these rules is to prevent (for example) profits being transferred from an individual to a corporation owned by him (or a member of his family). The anti-avoidance provisions therefore aim to redirect diverted profits to the individual concerned.

Salaried members

The rules on salaried members are designed to identify members whose conditions of service are more akin to an employment relationship than to self-employment. These rules apply only to UK LLPs, and not to partnerships or limited companies formed overseas.

In terms of partnership tax, where a person is treated as an employed member, they will be subject to PAYE and Class 1 National Insurance Contributions (NICs) on their LLP income. The LLP will also be subject to Class 1 NICs in respect of the salaried member’s remuneration, but will be able to claim a tax deduction for the cost of their employment. In effect, the payment to the member is treated as employment income for tax purposes.

A person is treated as a salaried member when all three of the following conditions are met:

Condition A

The individual provides services to the LLP in his or her capacity as a member, and it is “reasonable to expect” that the remuneration payable by the LLP for these services is wholly or substantially (presumed to be 80% or more) a “disguised salary”.

Disguised salary is remuneration that is fixed or, if variable, is not calculated by reference to, or is in practice unaffected by, the LLP’s overall profits or losses.

Individuals will be covered by this condition unless more than 20% of their variable remuneration is linked to the company’s overall profitability. It is not enough for it to be linked to the performance of the individual, branch or team.

Condition B

Condition B is that the mutual rights and duties of the members and the LLP do not give the member significant influence over the LLP’s affairs.

This is interpreted by HM Revenue & Customs (HMRC) to mean the role played by the individual and whether that individual is “in business” or simply “working for the company”.

Influence on one part or branch of the LLP, rather than the whole, is also insufficient. Many large partnerships and those with hierarchical or management structures are likely to find that only a few partners will escape this condition. HMRC has confirmed that influence does not necessarily mean sitting on the LLP board.

Condition C

Condition C is that the individual’s capital is less than 25% of the LLP’s disguised salary in the relevant tax year.

This is the amount the individual has invested under the LLP agreement, taking into account any subsequent changes. However, it does not include amounts that the member may withdraw, such as unused profits or short-term loans.

When a partner leaves or joins the partnership during the year, the capital contribution is prorated for the purposes of this test.

If either of these conditions is not met, the individual will continue to be treated as self-employed for tax purposes (and the tax payable on the partnership will therefore be only on the individual’s share of partnership income and expenses).

This factsheet is based on HMRC law and practice as at May 1, 2019. https://www.saffery.com/insights/publications/partnership-tax/

As a reminder, the creation of a Company incorporation abroad must be motivated by commercial or strategic necessity, as part, for example, of an expatriation project or to relocate the manufacture of products, a search for a location to facilitate logistics (notably import-export), proximity for human resources and raw materials, cost savings notably for warehousing, etc….

We hope these explanations provide a useful summary; they do not constitute legal or tax advice. We are by no means lawyers, and you should consult a tax and/or international trade lawyer before placing an order on our website.

“The LLP itself pays no tax on its profits. https://hillierhopkins.co.uk/faq/llp-v-limited-company-whats-best/#:~:text=An%20LLP%20allows%20its%20members,at%20the%20marginal%20rate%20applicable.

Tax in a limited liability company versus an LLP

One of the main differences between limited liability partnerships and LLPs is the treatment of tax. A limited liability company is completely separate from the people in the business, so for tax purposes this means :

A limited company pays tax in its own right, filing a corporation tax return and paying corporation tax on taxable profits.

Directors pay tax separately on the income they derive from the company. Their income may come from a salary paid to them by the company. If directors are also shareholders, they may also receive a share of the company’s profits in the form of dividends.

An LLP as an entity is not taxable, but the members are. So, no corporation tax return, and no corporation tax for an LLP. https://www.theaccountancy.co.uk/limited-company/whats-difference-llp-limited-company-7698.html#Tax%20in%20a%20limited%20company%20versus%20an%20LLP

“LLP: Taxation

Although in general law an LLP is treated as a body corporate, for tax purposes an LLP is normally treated as a partnership under the Income Tax (Business and Other Income) Act 2005 S863, S1273 of the Corporation Tax Act 2009.

Where an LLP carries on a trade, profession or other business with a view to making a profit:

all LLP activities are considered to be carried out as a partnership by its members (and not by the LLP as such)

anything done by, to or in connection with the LLP for the purposes of any of its activities shall be deemed to be done by, to or in respect of the members as partners, and the property of the LLP shall be deemed to be held by the members of the LLP.

An LLP must be transparent for tax purposes and, consequently, each partner is charged income tax or corporation tax on his share of the LLP’s income or gains as if he were a member of a partnership governed by the Partnerships Act 1890.

It follows that where an LLP carries on business with a view to profit, it may be considered a partnership in respect of all its activities, including those not carried on with a view to profit.

It is the persons registered as members of the LLP who carry on the business. If an LLP carries on an operation, each registered member is taxable on the income he or she derives from the LLP as business profits.” https://www.gov.uk/hmrc-internal-manuals/partnership-manual/pm131450

The company must have a registered office address in London; we provide this for €41 + VAT. per month, including digital mail management.

Company incorporation in Europe

Company incorporation in Europe is when you first apply to register a company in a different European country from the one in which the owner of the company is resident for tax purposes.

London society

“London society” is an expression that could refer to various aspects of social, economic and cultural life in London.

Here are a few areas in which we could explore this society:

History: London’s history, from Roman times to the present day, including landmark events such as the Great Plague, the Great Fire of London, and the Victorian period.

Culture and Arts: London is known for its rich cultural scene, with museums (such as the British Museum and Tate Modern), theaters (such as the West End), and cultural events (such as the Notting Hill Carnival).

Economy: London is a global financial center, with the City and Canary Wharf home to numerous international financial institutions.

Diversity: London is an extremely diverse city, with people from many ethnic, religious and cultural backgrounds.

Lifestyle: London’s different neighborhoods offer a multitude of lifestyles, from the chic districts of Kensington and Chelsea to more alternative areas like Camden.

Politics & Governance: London’s role as the political capital of the UK, with institutions such as the British Parliament and the Prime Minister’s residence in Downing Street.

Clavero Alban

Mon comte Revolut Business a été ouvert et opérationnel en seulement une demi-journée !!

L’accompagnement était parfait. Fluide et d’une efficacité redoutable, qui a rendu le processus très simple. Merci 🙏🏼

(Clavero Alban, Avis 100% réels, preuves à l’appui) 17/04/25

Wafiq Khemili

Exceptionnel

(Wafiq Khemili, Avis 100% réels, preuves à l’appui) 16/04/25

Sébastien Le Borgne

rapide et éfficace, au top, super merci, super service, le call est top en meet avec la personne qui nous aide

(Sébastien Le Borgne, Avis 100% réels, preuves à l’appui) 16/04/25

Leuz Ndiaye

Réactivité, professionnalisme, bon relationnel

(Leuz Ndiaye, Avis 100% réels, preuves à l’appui ) 15/04/25

Sébastien Le Borgne

ohhh super rapide en effet 🙂

(Sébastien Le Borgne, Avis 100% réels, preuves à l’appui ) 15/04/25

H. Maidouni

J'ai eu une interaction extrêmement agréable avec le service compliance.

La responsable a répondu à une question avec une rapidité et une efficacité exceptionnelles, ce qui m'a été très utile et m'a permis d'exécuter ce que je devais faire.

(H. Maidouni, Avis 100% réels, preuves à l’appui ) 03/04/25

Anne-so Dujardin

Une cliente satisfaite et fidèle ! Simple, fluide, pratique et bon rapport qualité-prix pour les services proposés et rendus.

Merci pour leur excellent service ! (Anne-so Dujardin, Avis 100% réels, preuves à l’appui ) 07/04/25

Nathalie MICHEL

J'ai toujours eu une réponse rapide de leur part. J'ai eu affaire au service technique et ils sont très serviables et prêts à me fournir les informations dont j'ai besoin. Je les recommande. (Nathalie MICHEL, Avis 100% réels, preuves à l’appui ) 04/04/25

Jean M.

Toujours excellent… Cette société a toujours offert un service impeccable ! J'avais une question aujourd'hui et Erick m'a répondu en 30 minutes (peut-être plus rapidement). À notre époque où il est de plus en plus difficile d'obtenir un bon service, c'est tellement agréable de pouvoir compter sur une entreprise comme service-société.com pour me soutenir. (Jean M., Avis 100% réels, preuves à l’appui ) 09/04/25

Société FTD Express

Rapide et efficace Sans attendre au téléphone, j'ai parlé à Erick qui a répondu à mes questions rapidement et efficacement. Extrêmement serviable. (Société FTD Express, Avis 100% réels, preuves à l’appui ) 04/04/25

Soïzic Mireur

Leur réactivité est excellente et les réponses d’un haut niveau…. et c'est la troisième fois !!! Leur concept de redynamisation d’une activité est génial, leur maîtrise de la procédure de dissolution par TUP transfrontalière est parfaite !!.. (Soïzic Mireur, Avis 100% réels, preuves à l’appui ) 02/04/25

Bruno Marin

Agence de création d'entreprise et de services associés de qualité supérieure. Ils mettent tout en œuvre pour répondre rapidement à toutes vos questions. (Bruno Marin, Avis 100% réels, preuves à l’appui ) 31/03/25

Patrick Schwartz

J'ai bénéficié de l'assistance de 2 personnes du service client et j'ai bénéficié d'un accompagnement exemplaire : rapide et professionnel. Fortement recommandé. (Patrick Schwartz) 20/03/25

Nordine B.

J'ai récemment fait appel à service-société pour l'immatriculation de ma nouvelle entreprise au Royaume-Uni, et j'ai été extrêmement impressionné par leur service. Dès le début, leur équipe a fait preuve d'un professionnalisme, d'une expertise et d'un soutien exceptionnels, rendant le processus fluide. Merci à toute l’équipe pour toute votre aide. (Nordine B., 31/03/25)

N. Coll

Le service client de service-societe.com a été très rapide et efficace. Le responsable du service TUP m'a vraiment bien expliqué la tup transfrontalière. Je suis très satisfait. Je recommande ce site à tous les dirigeants de société qui rencontrent de graves difficultés (N. Coll, 29/03/25)

David C.

Utile - J'ai trouvé le chargé de clientèle très sympa, respecteux, et très compétent sur les services fournis, y compris les avantages et inconvénients dans différents pays (David C., 27/03/25)

SAM

L'expérience a été merveilleuse Du début à la fin, le suivi a été formidable et extrêmement enrichissant. Tout a été excellent et soigné, de la création de l'entreprise aux moindres détails. La personne en charge de mon dossier m'a expliqué étape par étape tout ce qui concernait la création de la société, l'acheminement du courrier et tout le reste. Un service excellent, 10/10. Ils m'ont accompagné du début à la fin et m'ont traité avec professionnalisme. Merci à toute leur formidable équipe. (SAM, 25/03/25)

Groomies

« Parfait, Top. Nous apprécions votre service et aimerions continuer à collaborer avec vous » (Groomies, 19/03/25) Avis 100% réels, preuves à l’appui

Olivier BLIN

« Tout est fait pour la société et je vous en remercie. Le compte Revolut est ouvert et j'ai reçu ma carte de paiement. » (Olivier BLIN, 19/03/25) Avis 100% réels, preuves à l’appui

André Choite MBAMY

« Ma gratitude envers Service Société Je tiens à exprimer ma gratitude envers Service Société pour son professionnalisme, sa rapidité et sa réactivité. Bien que juriste et docteur en droit exerçant en cabinet d'avocat à Paris, j'ai été particulièrement impressionné par leur expertise et leur efficacité dans la création d'une LLP à Londres.

Tout au long du processus, cette société a fait preuve d'une écoute attentive, d'une grande compétence et d'une rigueur exemplaire, offrant un accompagnement personnalisé et de qualité. Leur maîtrise du sujet et leur engagement en font un partenaire de confiance.

Je recommande vivement Service Société à toute personne souhaitant créer une entreprise en toute sérénité, avec un service réactif, fiable et professionnel. » (André Choite MBAMY, 10/03/25) Avis 100% réels, preuves à l’appui

Alban Clavero

"Merci ! Incroyable réactivité (pray)" (Alban Clavero, 26/02/25) Avis 100% réels, preuves à l'appui

Duc Destin

"Merci pour votre gentillesse et pour votre professionnalisme sans faille🙏 " (Duc Destin, 03/02/2025), Avis 100% réels, preuves à l'appui

Tidadini Mehdi

"J'ai eu de mauvaises expériences par le passé, Je suis content de vous avoir trouvé, de votre réputation et de votre travail, c'est très rare. Je suis 100% satisfait de votre rapidité et qualité de service. " (Tidadini Mehdi, 03/02/2025), Avis 100% réels, preuves à l'appui

GEORGIEV TUP

« Super » (Nikolay GEORGIEV TUP, 22/01/25) Avis 100% réels, preuves à l’appui

Lucas PINOSA

« Je suis satisfait de vos prestations pour la création de ma société à Malte, service client au top » (Lucas PINOSA, 19/01/25) Avis 100% réels, preuves à l’appui

Benjamin Marciano

« Super merci beaucoup ! » (Benjamin Marciano, 14/01/25) Avis 100% réels, preuves à l’appui

MOUSSOUS Mohamed

"Bon travail" (MOUSSOUS Mohamed, 13/01/25) Avis 100% réels, preuves à l'appui

Solal Cacoub

"Super, aucuns problèmes, merci" (Solal Cacoub, 13/01/25) Avis 100% réels, preuves à l'appui

Joël MAMELOUK

"Merci beaucoup pour votre rapidité" (Joël MAMELOUK, 13/01/25) Avis 100% réels, preuves à l'appui

Hajji Nassim

« Je tiens à remercier toutes les personnes qui m'ont accompagné » (Hajji Nassim, 06/01/25) Avis 100% réels, preuves à l’appui

Morgan Belhadj

« Super, parfait, merci à vous et merci de votre patience, et surtout de votre gentillesse que vous avez eu envers moi parce que j’ai été très compliqué» (Morgan Belhadj, 04/01/25) Avis 100% réels, preuves à l’appui

Sandra MENDEZ

« Merci pour votre efficacité » (Sandra MENDEZ, 03/01/25) Avis 100% réels, preuves à l’appui

Birama Coly SARR

« C'est ok le compte Revolut a été ouvert et activé pour ma société Business Solutions Design LLP Encore merci Birama » (Birama Coly SARR, 24/12/24) Avis 100% réels, preuves à l’appui

Maryline

« Bonjour, chatgpt m’a conseillé votre site pour créer une holding en Irlande. » (Maryline, Belgique, 24/12/24) Avis 100% réels, preuves à l'appui

Birama Coly SARR

"Je suis très satisfait de vos services, encore merci pour vos documents" (Birama Coly SARR, 12/12/24) Avis 100% réels, preuves à l'appui

Sandra MENDEZ

« Merci pour votre efficacité. » (Sandra MENDEZ, 05/12/24) Avis 100% réels, preuves à l’appui

Cheriff CHOUABBIA

« Vous faites un très bon travail » (Cheriff CHOUABBIA, 27/11/24) Avis 100% réels, preuves à l’appui

SAMB Alassane

Fondateur de l'enseigne Pizzas WOODIZ : « TOP, parfait, super, réactif, bonnes infos, rapide » (SAMB Alassane, 23/11/24) Avis 100% réels, preuves à l’appui

Philippe BORMS

Fondateur de l'enseigne EAT TO EAT : « Je suis satisfait de vos services » (Philippe BORMS, 28/11/24) Avis 100% réels, preuves à l’appui

Hakim Benotmane

Fondateur de l'enseigne en franchise Nabab Kebab et patron dans l’émission sur M6 « Patron Incognito » : « Top, parfait 👍, très très bien » (Hakim Benotmane, 23/11/24) Avis 100% réels, preuves à l’appui

Jérôme EBELLA « Kenzy »

Rappeur, éditeur, producteur et agent artistique, manager du groupe Ministère A.M.E.R. et fondateur, avec Frédéric Bride de la société Secteur Ä. Les deux rappeurs du groupe Ministère A.M.E.R., Stomy Bugsy et Passi, auront ensuite de nouveaux managers : « Je suis satisfait de vos services » (Jérôme EBELLA « Kenzy », 28/11/24) Avis 100% réels, preuves à l’appui

Jean TOFFIN

« Merci beaucoup pour votre diligence pour l’acquisition de la société. » (Jean TOFFIN, 28/11/24) Avis 100% réels, preuves à l’appui

CHOITE MBAMY Fochada

« Wowwww !!! Je vais donner votre contact. Magnifique !! » (CHOITE MBAMY Fochada, 02/11/24) Avis 100% réels, preuves à l’appui

Djilali Sadki

« Merci pour la réactivité et l’efficacité »(Djilali Sadki, 01/11/24) Avis 100% réels, preuves à l’appui

PICCINELLI David

« Propre et efficace....bravo! J ai d autres besoins on va en parler » (PICCINELLI David, 01/11/24) Avis 100% réels, preuves à l’appui

Bruno Péreira

« Bonjour, J'ai un retour de la banque le document a été validé. Merci » (Bruno Péreira, 18/10/24) Avis 100% réels, preuves à l’appui

Malik LIFA

«Merci de votre réactivité et votre professionnalisme » (Malik LIFA, 14/10/24) Avis 100% réels, preuves a l’appui

MAICAS Salomon

« Vous êtes super merci👍 » (MAICAS Salomon, 02/10/24) Avis 100% réels, preuves à l’appui

BONFILS Ludovic

« Parfait, rapide !!» ( BONFILS Ludovic, 24/09/24) Avis 100% réels, preuves à l’appui

Nacim Mahtallah

« Très satisfait » (Nacim Mahtallah, 05/09/24) Avis 100% réels, preuves à l’appui

Hervé LOUIT

« Super vous êtes au top, vous êtes très pro et sérieux » (Hervé LOUIT, 05/09/24) Avis 100% réels, preuves à l’appui

Frédéric HUGON

« 👍super » (Frédéric HUGON, 30/08/24) Avis 100% réels, preuves à l’appui

Jean-Claude DUCOUP

« Je suis satisfait de vos services! » (Jean-Claude DUCOUP, 16/08/24) Avis 100% réels, preuves à l’appui

Sébastien DROIT

« Juste parfait ! À la vue de ce premier projet je ne peux que vous recommander ! » (Sébastien DROIT, 13/08/24) Avis 100% réels, preuves à l’appui

Anthony BERNA

« super je suis très content de votre travail 😊😊😊 » (Anthony BERNA, 13/08/24) Avis 100% réels, preuves à l’appui

Benjamin MARCIANO

« Magnifique, merci » (Benjamin MARCIANO, 18/07/24) Avis 100% réels, preuves à l’appui

ELAMRI Faouzi

"C'est parfait" (ELAMRI Faouzi, 20/06/24) Avis 100% réels, preuves à l'appui

Alexandra CLUZEL

« Merci super c’est parfait » (Alexandra CLUZEL, 13/06/24) Avis 100% réels, preuves à l’appui

Gérard Massonne

« Parfait merci 🙏 » (Gérard Massonne, 12/06/24) Avis 100% réels, preuves à l’appui

Blanchard Euloge

"J'ai apprécié votre travail" (Blanchard Euloge, 04/06/24) Avis 100% réels, preuves à l'appui

Jérôme BRUY

« Merci d’avoir créé ma société à Malte. De plus, J’ai pu ouvrir mon compte HSBC grâce à votre service d’introduction bancaire, merci pour tout !… » (Jérôme BRUY, 01/06/24) Avis 100% réels, preuves à l’appui

Henri TALBOTIER

« Parfait Merci beaucoup ! »(Henri TALBOTIER, 29/05/24) Avis 100% réels, preuves à l’appui

« Kenzy » ex Ministère A.M.E.R, groupe de Hip-Hop

« Je suis très très content de vos services » 27/05/24 (« Kenzy » ex Ministère A.M.E.R, groupe de Hip-Hop) Avis 100% réels, preuves à l’appui

DESTIN Abonckelet

"Vous faites vraiment un bon boulot, merci pour votre professionnalisme" (DESTIN Abonckelet, 25/05/24) Avis 100% réels, preuves à l'appui

Ilias Moutani

« Franchement je suis très content, dès qu’on me demande je vous conseil » (Ilias Moutani, 09/05/24)

Mohamed BESSA

"C'est parfait, je vous fais confiance" (Mohamed BESSA, 07/05/24) Avis 100% réels, preuves à l'appui

SAINT-PRIX Pradeep

"Je suis très satisfait de la réactivité pour la holding. Je vais continuer à travailler avec vous. Top, merci encore à vous" (SAINT-PRIX Pradeep, 02/05/24) Avis 100% réels, preuves à l'appui

Dominique MARTELLA

« Très content de la création rapide , je vous en remercie » (Dominique MARTELLA, 25/04/24) Avis 100% réels, preuves à l’appui

Francois Pinguet

« Vous avez déjà immatriculé ma société …!!! C’est génial !! » (Francois Pinguet, 23/04/24) Avis 100% réels, preuves à l’appui

Samira Maouda

« Merci d’avoir créé notre société, pour votre aide et le suivi » (Samira Maouda, 23/04/24) Avis 100% réels, preuves à l’appui

Ilias Moutani

« C’est parfait merci beaucoup pour tout » (Ilias Moutani, 16/04/24) Avis 100% réels, preuves à l’appui

TASSELLI Amael,

"Super merci" (TASSELLI Amael, 16/04/24) Avis 100% réels, preuves à l'appui

ROIKONEN

(ROIKONEN , 25/03/24) Avis 100% réels, preuves à l'appui

Anne-Sophie Zerbib

« Formidable ! Je suis ravie de travailler avec vous. J'apprécie votre efficacité 👍 » (Anne-Sophie Zerbib, 25/03/24) Avis 100% réels, preuves à l’appui

Anaelle JUGE

"Super merci génial!! Toujours aussi efficace! » Anaelle JUGE, 19/03/24) Avis 100% réels, preuves à l'appui

Aaron Cohen Azran

« Très satisfait » (Aaron Cohen Azran, 11/03/24) Avis 100% réels, preuves à l’appui

Thierry Krieger

« Merci pour votre efficacité. » (Thierry Krieger, 01/03/24) Avis 100% réels, preuves à l’appui

Omar Hadjadj

« Parfait » (Omar Hadjadj, 02/03/24) Avis 100% réels, preuves à l’appui

Lionel LAWSON

« Je suis satisfait de vos services qui ont été très utiles pour moi. Je vous remercie de votre professionnalisme, de votre célérité et je n’hésiterai pas à transmettre vos coordonnées. » (Lionel LAWSON, 01/03/24) Avis 100% réels, preuves à l’appui

Florian MEUNIER

"OK top. Merci beaucoup pour votre professionnalisme. Vous êtes un top dans votre domaine car vous êtes quelqu'un de direct, j'aime beaucoup" (Florian MEUNIER, 28/02/24) Avis 100% réels, preuves à l'appui

William Bailly

« Très satisfait » (William Bailly, 26/02/24) Avis 100% réels, preuves à l’appui

Rabah Medjane

« Je suis très satisfait de vos services surtout de votre réactivité. Je me fais plaisir de partager votre Société. » (Rabah Medjane, 26/02/24) Avis 100% réels, preuves à l’appui

Avis service-societe.com

« Je tenais à vous remercier pour votre travail et votre professionnalisme. Votre expertise est très appréciée, 👍et je n'hésiterai pas à faire appel à vos services pour de futures prestations dans votre domaine de compétence. Merci encore. » (Wilfried Azade, 07/10/24) Avis 100% réels, preuves à l’appui

Guy BARBET

"AU TOP" (Guy BARBET, 19/02/24) Avis 100% réels, preuves à l'appui

Yannick LE CORRE

"Merci bcp. Travail très efficace de votre part" (Yannick LE CORRE, 12/02/24)

Florian MEUNIER

« J’ai une entière confiance en vous et en votre professionnalisme. » (Florian MEUNIER, 31/01/24) Avis 100% réels, preuves à l’appui)

Medjane Rabah

« Merciiii beaucoup » (Medjane Rabah, 23/01/24) Avis 100% réels, preuves à l’appui

Valérie TASSELI

"Génial" (Valérie TASSELI, 16/01/24) Avis 100% réels, preuves à l'appui

Vincent CHEVALIER

"C'est parfait, merci" (Vincent CHEVALIER, 09/01/24) Avis 100% réels, preuves à l'appui

Georgios Bouronikos

« Bonjour 🙂 vous êtes un vendeur adorable 🙂 » (Georgios Bouronikos, 05/01/24) Avis 100% réels, preuves à l’appui

Robin NICOLET

« Parfait merci pour votre professionnalisme à 100 % croyez moi je parle de vous a beaucoup de gens. Vous méritez que votre société puisse avoir des clients énormes, c’est sincère et je le pense. » (Robin NICOLET, 14/12/23) Avis 100% réels, preuves à l’appui

Daniel GOEDRAAD

"Merci pour votre patience👍💪👏 excellent et merci" (Daniel GOEDRAAD, 11/12/23) Avis 100% réels, preuves à l'appui

CRETU Florin

« Merci pour vos services » (CRETU Florin, 11/12/23) Avis 100% réels, preuves à l’appui

Konstantatos Nicolas

« Parfait et bravo » (Konstantatos Nicolas, 06/12/23) Avis 100% réels, preuves à l’appui

Mostapha EL ASRi

« Merci, au top »Mostapha EL ASRi, 06/12/23) Avis 100% réels, preuves à l’appui

Dominique BIDAUD

« Très satisfait » (Dominique BIDAUD, 20/11/23) Avis 100% réels, preuves à l’appui

Xavier Rossignol

« Parfait merci » ( Xavier Rossignol, 10/11/23) Avis 100% réels, preuves à l’appui

Bilal DERARD

« On est ravis de vos service merci encore ! » (Bilal DERARD, 06/11/23) Avis 100% réels, preuves à l’appui

Lionel LAWSON

« Merci pour vos services rendus » (Lionel LAWSON, 27/10/23) Avis 100% réels, preuves à l’appui

Ilias MOUTANI

"Vous travaillez de manière pro, c'est rare👍 " (Ilias MOUTANI, 19/10/23) Avis 100% réels, preuves à l'appui

Giorgios Bouronikos

« Merci beaucoup pour votre disponibilité et aide. » (Giorgios Bouronikos, 06/10/23) Avis 100% réels, preuves à l’appui)

Kamel Hadji

« Je vous ai conseillé, on ne peut pas vous enlever votre rapidité (Kamel Hadji, 02/10/23) Avis 100% réels, preuves à l’appui

Albéric Bonjean

"OK génial merci" (Albéric Bonjean, 27/09/23) Avis 100% réels, preuves à l'appui

David Zachara

« ok super merci excellent» (David Zachara, 26/09/23) Avis 100% réels, preuves à l’appui

Anne-Laure DUPORGE

« Sachez que je suis complètement satisfaite de vos services, votre réactivité et vos explications ont répondu à nos demandes pour la création de notre société et je n'oublie pas ce genre de choses 🙂 , j’ajoute que vous êtes excellent dans ce que vous faites » (Anne-Laure DUPORGE, 23/09/23) Avis 100 % réels, preuves à l’appui

Robin Nicolet

« Nous sommes satisfait du service qui a été effectué et nous vous en remercions » (Robin Nicolet, 23/09/23) Avis 100 % réels, preuves à l’appui

William Bailly

« je suis très satisfait de votre service, nous allons continuer notre collaboration, je vais donc faire ma succursale française, encore un grand merci pour la collaboration votre professionnalisme ne peut que vous honoré » (William Bailly, 21/09/23) Avis 100% réels, preuves à l’appui

Kamel Hadji

« Très bien rapide et efficace » (Kamel Hadji, 15/09/23) Avis 100% réels, preuves à l’appui

Wilfried AZADE

"C'est TOP" (Wilfried AZADE, 14/09/23) Avis 100% réels, preuves à l'appui

Kamel Hadji

« Super top merci » (Kamel Hadji, 06/09/23) Avis 100% réels, preuves à l’appui

Yvan ERBS

« Vous avez été parfait, merci, très satisfait » (Erbs Yvan, 06/09/23) Avis 100% réels, preuves à l’appui

GIMEL Laurent

"Super" (GIMEL Laurent, 01/09/23) Avis 100% réels, preuves à l'appui

Ilias Moutani

« OK top, bien reçu, c’est parfait 👍 , merci pour votre réactivité » (Ilias Moutani, 25/08/23) Avis 100% réels, preuves à l’appui

Géoffroy PAICHELER

"Bravo pour votre réactivité, Je suis content de vos prestations" (Géoffroy PAICHELER, 23/08/23) Avis 100% réels, preuves à l'appui

Bruno SCARPA

"Parfait merci, top" (Bruno SCARPA, 17/08/23) Avis 100% réels, preuves à l'appui

Mohamed Z.

"La réunion en ligne s'est bien déroulée. Personne très sympa. Nous attendons les documents pour la BG Garantie Bancaire pour pouvoir effectuer le onboarding. Merci à vous" (Mohamed Z., 17/08/23) Avis 100% réels, preuves à l'appui

Mohamed ZEGHIB

"Très bien" (Mohamed ZEGHIB, 14/08/23) Avis 100% réels, preuves à l'appui

Franck Boizot

« Super » (Franck Boizot, 12/08/23) Avis 100% réels, preuves à l’appui

Adrien LOMBARD

« OK parfait » (Adrien LOMBARD, 08/08/23) Avis 100% réels, preuves à l’appui

Paul-marie Vouvou

« Génial, merci beaucoup » (Paul-marie Vouvou, 07/08/23) Avis 100% réels, preuves à l’appui

Ryann Guillonnet

« Génial, merci » (Ryann Guillonnet, 21/07/23) Avis 100% réels, preuves a l’appui

Guillaume Chocat

« Parfait merci bien » (Guillaume Chocat, 16/07/23) Avis 100% réels, preuves à l’appui

Adrien Lombard

« Merci beaucoup » (Adrien Lombard, 11/07/23) Avis 100% réels, preuves à l’appui

Daniel Plastivene

« Merci d'avoir coordonné tout ça, sincèrement, je n'hésiterai pas à retourner vers vous pour d'autres projets » (Daniel Plastivene, 06/07/23) Avis 100% réels, preuves à l’appui

Stéphane Dupain

« c'est propre. Je n'ai pas de remarque et vous fait confiance.» (Stéphane Dupain, 06/07/23) Avis 100% réels, preuves a l’appui

William Bailly

« j'ai reçu ma carte hier » (William Bailly, 06/07/23) Avis 100% réels, preuves à l’appui

Zuka Jelena

« Super merci pour votre réactivité » (Zuka Jelena, 05/07/23) Avis 100% réels, preuves à l’appui

Bilal DERARD

« Super nous somme ravis, Merci pour tout. Je tenais à vous en informer pour la qualité et la rapidité de vos services. Je vous informe aussi que je compte encore faire appel à vos services pour la création de mes succursale en Belgique et en France.» (Bilal DERARD, 05/07/23) Avis 100 % réels, preuves à l’appui

Paul GLATIGNY

« Bonjour, pour la qualité de vos services parfait. merci par avance. » (Paul GLATIGNY, 23/06/23) Avis 100% réels, preuves à l’appui

Robin David NICOLET

« Je vous remercie 🙏🙏🙏 Nous sommes ici à la bonne place et au bon moment avec les bonnes personnes 🙏 , Merci beaucoup pour votre travail. C'est un travail rapide et de qualité !!! Encore une fois bravo pour votre professionnalisme et votre rapidité» (Robin David NICOLET, 22/06/23 et 26/06/23) Avis 100% réels, preuves à l’appui

Anne-Laure DUPORGE

« Vous avez toujours été réactif et efficace depuis le départ, et là votre geste me prouve que l'on ne s'est pas trompés. Vous travaillez sur le long terme et c'est parfait car nous recherchons la même chose » (Anne-Laure DUPORGE, 22/06/23) Avis 100% réels, preuves à l’appui

David SEROUSSI

"Merci pour votre efficacité " (David SEROUSSI, 16/06/2023) Avis 100% réels, preuves à l'appui

Henri TALBOTIER

« Merci beaucoup, c’est parfait, ravi de votre service ! » (Henri TALBOTIER, 14/06/23) Avis 100% réels, preuves à l’appui

William Bailly

« je vous remercie j'ai pu enfin ouvrir mon compte bancaire je vais avoir le numéro dans l'après-midi je pourrai donc effectuer les premières rentrées d'argent, merci à vous » (William Bailly, 13/06/23) Avis 100% réels, preuves à l’appui

Henri TALBOTIER

« merci beaucoup c’est génial » (Henri TALBOTIER, 12/06/23) Avis 100% réels, preuves à l’appui

Alexandra CLUZEL

« Super, merci, nickel » (Alexandra CLUZEL, 12/06/23) Avis 100% réels, preuves à l’appui

Aymen Bayèche

« OK parfait » (Aymen Bayèche, 07/06/23) Avis 100% réels, preuves a l’appui

M. Essombe

« Très satisfait, Merci pour votre disponibilité. » (M. Essombe, 30/05/23) Avis 100% réels, preuves à l’appui

Philippe LACOSTE

"Nickel, merci de votre aide" (Philippe LACOSTE, 29/05/23) Avis 100% réels, preuves à l'appui

HENRI TALBOTIER

« Merci beaucoup » ( HENRI TALBOTIER, 27/05/23) Avis 100% réels, preuves à l’appui

Ralph Pinto

« Parfait, merci beaucoup » (Ralph Pinto, 26/05/23) Avis 100% réels, preuves à l’appui

Elbak Soule

« Merci, vous êtes les meilleurs ! » (Elbak Soule, 25/05/23) Avis 100 réels, preuves à l’appui

Eric BREDA

« Parfait merci » (Eric BREDA, 23/05/23) Avis 100% réels, preuves à l’appui

Mustapha Gherras

« Fantastique » (Mustapha Gherras, 11/05/23) Avis 100% réels, preuves à l’appui

Hassen LASSOUED

« Good job 👍 Professionnalisme 👍 Merci » (Hassen LASSOUED, 10/05/23) Avis 100% réels, preuves à l’appui

Lionel LAWSON

« Je suis satisfait des services rendus par vos services.. nickel, la société est opérationnelle. » (Lionel LAWSON, 10/05/23) Avis 100% réels, preuves à l’appui

Elbak SOULE

"Superbe nouvelle ! Merci beaucoup , très content 😊 Parfait ! 👍 et merci pour le suivi " (Elbak SOULE, 28/04/23) Avis 100% réels, preuves à l'appui

Ben Salmi

« Très bien, très sérieux à recommander » (Ben Salmi, 24/04/23) Avis 100% réels, preuves à l’appui

Stéphane DUPAIN

« Je vous remercie de votre sérieux » ( Stéphane DUPAIN, 17/04/23) Avis 100% réels, preuves à l’appui

Mohammed Réda Malouda

« je suis très content de votre prestation jusqu’à présent rapidité et professionnalisme » (Mohammed Réda Malouda, 13/04/23) Avis 100% réels, preuves à l’appui

Nassim Zekhnini

« Super service » (Nassim Zekhnini, 08/04/23) Avis 100% réels, preuves à l’appui

D. Seroussi

« Au plaisir de perpétuer notre relation professionnelle »(D. Seroussi, 03/04/23) Avis 100% réels, preuves à l’appui

Badi Garnaoui

« C'est bon la banque à accepter les virements grâce à votre partenaire pour l’introduction bancaire, ils viennent de me faire un transfert vers la Tunisie » (Badi Garnaoui, 03/04/23) Avis 100% réels, preuves à l’appui

Achraf Zelmat

« La réactivité du service est bluffante, on n'avait plus l'habitude. Les engagements sont tenus. » (Achraf Zelmat, 30/03/23) Avis 100% réels, preuves à l’appui

Nicolas

« un simple mot pour vous remercier du service courtois et professionnel dont vous nous avez fait bénéficier, Il nous fera plaisir de vous recommander auprès de notre entourage et nous tenions à vous l’écrire Au plaisir d’une autre collaboration ensemble Salutations » (Nicolas) Avis 100% réels, preuves à l’appui

SIPPC LLP

« Temps record de création de la société, très attentif, répond sans gêne a tous nos questions, je recommande vraiment » (SIPPC LLP) Avis 100% réels, preuves à l’appui

Nassim Zekhnini

« Un grand merci » (Nassim Zekhnini, 27/03/23) Avis 100% réels, preuves à l’appui

Redjala Adel

« Super merci beaucoup » (Redjala Adel, 27/03/23) Avis 100% réels, preuves à l’appui

Benadda Kouider

« Un grand merci ! » (Benadda Kouider, 22/03/23) Avis 100% réels, preuves à l’appui

Thierry KRIEGER

"Top, Super merci beaucoup" (Thierry KRIEGER, 20/03/23) Avis 100 % réels, preuves à l'appui

Samir Bourouf

« Merci pour votre réactivité, vous êtes au top » (Samir Bourouf, 16/03/23)

Roland Garcia

« Merci pour vos diligences » (Roland Garcia, 11/03/23) Avis 100% réels, preuves à l’appui

Olivier Mehdi

« Supeeer, merci » (Olivier Mehdi, 03/03/23) Avis 100% réels, preuves à l’appui

LIMA Anthony

"Super merci beaucoup" (LIMA Anthony, 28/02/23) Avis 100% réels, preuves à l'appui

Christian EL DEBS

"Parfait merci beaucoup" (Christian EL DEBS, 28/02/23) Avis 100% réels, preuves à l'appui

Willy L.

« l’accompagnement est vraiment au top ! » (Willy L. , 24/02/23) Avis 100% réels, preuves à l’appui

Kouassi Aimé Malanhoua

« Je suis satisfait du service rendu. Bien à vous. » (Kouassi Aimé Malanhoua, 16/02/23) Avis 100% réels, preuves à l’appui

Samir MANI

"Merci encore pour votre réactivité, ça m'aide beaucoup" (13/02/23, Samir MANI) Avis 100% réel, preuve à l'appui

Damien Léonetti

« Je suis ravi, je vous remercie » (Damien Léonetti, 04/02/23) Avis 100% réels, preuves à l’appui

ZIATA Amirouche

« Je viens de recevoir le certificat d’enregistrement de la société , Je vous remercie pour votre professionnalisme » (ZIATA Amirouche. 02/02/23) Avis 100% réels, preuves à l’appui

Delphine Picagne

« vous êtes parfait et satisfait de vos services. Merci » ( Delphine Picagne, 27/01/23) Avis 100% réels, preuves à l’appui

Nicolas Coll

"Réponse de la banque : Le service conformité a validé votre dossier, votre compte est bien ouvert. Merci pour votre confiance." (Nicolas Coll, 19/01/23)

Mukandila Mujinga

« Super » (Mukandila Mujinga, 18/01/23) Avis 100% réels, preuves à l’appui

Willy L.

« Merci pour l’accompagnement » (Willy L. , 16/01/23) Avis 100% réels, preuves à l’appui

Elisabete De Sousa

"Génial" (16/01/23, Elisabete De Sousa) Avis 100% réels, preuves à l'appui

Dominique MICHEL

"Merci beaucoup...compte société" (Dominique MICHEL, 11/01/23) Avis 100% réels, preuves à l'appui

Gregory Arm

« Merci beaucoup, très appréciable » (Gregory Arm, 09/01/23) Avis 100% réels, preuves à l’appui

Julian Sailley

« Top ! Super ! » (Julian Sailley, 03/01/23) Avis 100% réels, preuves à l’appui

Farès Azzoug

«Merci beaucoup, je suis totalement satisfait de la prestation » (Farès Azzoug, 28/12/22) Avis 100% réels, preuves à l’appui

Touradj Backhtiar

« Très bien, merci beaucoup » (Touradj Backhtiar, 28/12/22) Avis 100% réels, preuves à l’appui

Laurent Quéhen

« Je suis très satisfait de la rapidité de la mise en place de la société en GB et de la disponibilité ainsi que des conseils avisés d’Erick .Je recommande ! » (Laurent Quéhen, 24/12/22) Avis 100% réels, preuves à l’appui)

Farès Azzoug

« super je vous remercie 🙏 » (Farès Azzoug, 23/12/22) Avis 100% réels, preuves à l’appui

Aykel Mejri

« Parfait » (Aykel Mejri, 20/12/22) Avis 100% réels, preuves à l’appui

Yanis Taferand

« Vous travaillez vraiment a toute heure Franchement Bravo » (Yanis Taferand, 06/12/22) Avis 100% réels, preuves à l’appui

CY

« La banque vient de me contacter, merci » (CY, 15/12/22) Avis 100% réels, preuves à l’appui

Richard Pascal

"Nous avons été contents de votre accompagnement et de votre professionnalisme" Richard Pascal, (13/12/22) Avis 100% réels, preuves à l'appui

AGC Financement

« Super, c’est une bonne nouvelle, je suis très satisfait, j’ai reçu les documents » (Alexandre Dauriac, 12/12/22) Avis 100% réels, preuves à l’appui

Mounguengue Goma Franky

« merci, c’est un plaisir de trouver une franche collaboration avec vous » (Mounguengue Goma Franky, 11/12/22) Avis 100% réels, preuves à l’appui

Léo Dulice

"Parfait, t'es un chef, merci" (Léo Dulice, 09/12/22) Avis 100% réels, preuves à l'appui

AGC Financement

Nouvelle satisfaction « Parfait » (AGC Financement, le 09/12/22) Avis 100% réels, preuves à l’appui

Yanis TAFERAND

"Très satisfait, merci" (Yanis TAFERAND, 02/12/22) Avis 100% réels, preuves à l'appui

Corinne YOËL

"Super vous êtes au top! Merci" (Corinne YOËL, 24/11/22) Avis 100% réels, preuves à l'appui

Dominique MICHEL

"Parfait, merci beaucoup" (Dominique MICHEL, 24/11/22) Avis 100% réels, preuves à l'appui

Tachefine AJDIR

"Merci 👍 c'est très rapide" (Tachefine AJDIR, 23/11/22) Avis 100% réels, preuves à l'appui

C. YOËL

« Merci infiniment » (C. YOËL, 22/11/22) Avis 100% réels, preuves à l’appui

Mdioui Mohamed

« Merci pour vos services, merci pour le travail que vous avez effectué, vous avez fait le travail que je vous est demandé. Je vous recommanderai avec conviction à d'autres personnes. Cordialement » (Mdioui Mohamed, 11/11/22) Avis 100% réels, preuves à l’appui

Jérôme BOLAND

"Un grand merci" (Jérôme BOLAND, 08/11/22) Avis 100 % réels, preuves à l'appui

Erwan DELBART

"Parfait merci, on est tous satisfait 🙂 on ouvre le compte en ligne actuellement" (Erwan DELBART, 07/11/22) Avis 100% réels, preuves à l'appui

A. GHASSANI

"je suis très satisfait" (A. GHASSANI, 04/10/22) Avis 100% réels, preuves à l’appui

Etienne Mbaussègue

« Merci beaucoup, je vous suis infiniment reconnaissant » ( Etienne Mbaussègue, 31/10/22) Avis 100% réels, preuves à l’appui)

El Debs Christian

« Parfait merci beaucoup » (El Debs Christian, 29/10/22) Avis 100% réels, preuves à l’appui

Daniel MOUZITA

« Merci pour les documents et le travail fait. » (Daniel MOUZITA, 27/10/22) Avis 100% réels, preuves à l’appui)

Samir MANI

"Super, merci beaucoup" (Samir MANI, 25/10/22) Avis 100% réels, preuves à l'appui

Nino Paganelli

"Impeccable" (Nino Paganelli, 25/10/22) Avis 100% réels, preuves à l'appui

Guillaume GABILLET

« oui très bien ça m'a enlevé pas mal de problème ! Parfait, merci à vous »

(Guillaume GABILLET, 18/10/22) Avis 100 % réels, preuves à l’appui

HASSANE Adel

"Vous avez fait votre travail, je vous remercie pour vos services, vous êtes irréprochables, "

(HASSANE Adel, 13/10/22) Avis 100% réels, preuves à l'appui

Bilal ZIANE

« on avance, avec le compte bancaire physique on peut démarrer l'activité sur de bons rails avec votre assistance, merci infiniment »

(Bilal ZIANE, 10/10/22) Avis 100% réels, preuves à l’appui

Florian SKERRA

"Votre travail a été très bien fait et je vous remercie de la gentillesse que vous avez accordé à l'élaboration d'une solution pour avancer à chacune des étapes malgré la complexité de la situation"

(Florian SKERRA, 07/10/22) Avis 100% réels, preuves à l'appui

Adel HASSANE

"Parfait...excellent"

(Adel HASSANE, 07/10/22) Avis 100% réels, preuves à l'appui

Dominique ABAD

« Merci beaucoup pour la qualité de votre travail »

(Dominique ABAD, 06/10/22) Avis 100% réel, preuves à l’appui

David ZACHARA

« Merci Top… Super… ouverture de compte »

(David ZACHARA, 30/09/22) Avis 100% réels, preuves à l’appui

Alexandre Delaunay

« Impeccable... merci pour la création de la société !»

(Alexandre Delaunay, 29/09/22) Avis 100% réels, preuves à l’appui

Pascal Lusci

« Top merci à vous »

(Pascal Lusci, 28/09/22) Avis 100% réels, preuves à l’appui

Florian SKERRA

"C'est parfait"

(Florian SKERRA, 22/09/22) Avis 100% réels, preuves à l'appui

Elbak SOULE

Merci beaucoup pour ce boulot de grande qualité. J'en suis ravis et très satisfait. Merci à vous ! » (Elbak SOULE, 20/09/22) Avis 100% réels, preuves à l’appui)

RARBI Abdel-Magid

"Parfait"

(RARBI Abdel-Magid, 16/09/22) Avis 100 % réels, preuves à l’appui

Karim MESSAOUDI

« Merci pour votre service et votre sérieux »

(Karim MESSAOUDI, 16/09/22) Avis 100 % réels, preuves à l’appui

Elbak Soule

"Merci beaucoup pour votre réactivité et votre disponibilité."

(Elbak Soule, 15/09/22) Avis 100 % réels, preuves à l'appui

Guy-Maixent Onga-Nkwenkeu

« Je connais la qualité de votre travail…depuis que j'ai eu mes déboires avec ma banque j'ai fait appel à plusieurs structures et votre compagnie s'est révélée être la plus professionnelle »

(Guy-Maixent Onga-Nkwenkeu, 26/08/22) Avis 100% réels, preuves à l’appui

Ryann Guillonnet

« Niquel, le compte est bien créé 🙏 »

(Ryann Guillonnet, 14/09/21) Avis 100% réels, preuves à l’appui

Ryann GUILLONNET

« Génial !! Merci beaucoup »

(Ryann GUILLONNET, 13/09/22) Avis 100 % réels, preuves à l’appui

Dominique ABAD

« Je vous remercie pour votre aide et votre sérieux »

(Dominique ABAD, 12/09/22) Avis 100 % réels, preuves à l’appui

Alain DECANT

"Très satisfait"

(Alain DECANT, 01/09/22) Avis 100% réels, preuves à l'appui

Jean-Philippe VERM

« Rapidité… efficacité !! Toutes mes félicitations »

(Jean-Philippe VERM, 19/08/22) Avis 100 % réels, preuves à l’appui

Guy-Maixent Onga-Nkwenkeu

« J’ai bien ouvert mon compte bancaire à la Lloyds, je vous remercie »

(Guy-Maixent Onga-Nkwenkeu), 17/08/22) Avis 100 % réels, preuves à l’appui

Laurent CACCAMO

"Merci de votre implication efficace comme toujours"

(Laurent CACCAMO, 16/08/22) Avis 100 % réels, preuves à l'appui

Salif

« Nous sommes satisfaits de la création de la société »

(Salif, 10/08/22) Avis 100% réel, preuve à l’appui

Stéphane Baldacchino

« Je suis bien content de connaître votre entreprise »

(Stéphane Baldacchino, 10/08/22) Avis 100% réel, preuve à l’appui

Patrick FOVEZ

« Bravo, rapide et efficace ! Parfait, merci. Avoir un interlocuteur français et à l'écoute est très rassurant. »

(Patrick FOVEZ, 05 août 22) Avis 100% réel, preuve à l’appui

Daniel Mouzita

Très satisfait du traitement et de la réactivité.

(Daniel Mouzita, 18/07/22) Avis 100% réel, preuve à l’appui

Jacques Lalou

Service 5 étoiles (08/07/22)

Avis 100 % réels, preuves à l'appui

Mohamed Bessa

Parfait 👍 (11/04/22)

Avis 100 % réels, preuves à l'appui

Hakim S

Très professionnel, réactif et disponible surtout c’est important 👍 (24/03/22)

Avis 100 % réels, preuves à l’appui

Mat.

Nous sommes satisfait de la rapidité de la création de société (24/03/22)

Avis 100 % réels, preuves à l’appui

Boudairon

Je suis satisfaite des services de Service-societe, j'ai pu créer une société à l'étranger rapidement avec un bon rapport qualité/prix. Il y a un contact en langue française, ce qui est très appréciable. (24/03/22)

Avis 100 % réels, preuves à l’appui

Steeves Sfez

Merci pour votre réactivité votre diligence, votre sympathie, votre professionnalisme. J'avoue avoir été bluffé. Je vous promets beaucoup de retour (24/03/22)

Avis 100 % réels, preuves à l’appui

Guillaume Gabillet

C'est bon, extrait k-bis OK,

Merci pour votre professionnalisme.

A bientôt Guillaume (18/03/22)

Avis 100 % réels, preuves à l’appui

Jean-Marc S.

J'ai bien mon compte à la Lloyds (27/01/22)

Avis 100 % réels, preuves à l’appui

Mourad

Oui j'ai le RIB, TOP. (27/01/22)

Avis 100 % réels, preuves à l’appui

Bertrand P

J'ai bien mon compte en banque. Parfait merci (27/01/22)

Avis 100 % réels, preuves à l’appui

HC

Merci beaucoup pour votre réactivité (26/01/22)

Avis 100 % réels, preuves à l’appui

Raphaël V.

Merci Bien reçu (25/01/22)

Avis 100 % réels, preuves à l’appui

Hélias

Parfait (25/01/22)

Avis 100 % réels, preuves à l’appui

SO.

Good job (20/01/22)

Avis 100 % réels, preuves à l’appui

Raphaël V.

Je suis satisfait (19/01/22)

Avis 100 % réels, preuves à l’appui

Sofiane O

Parfait, merci (17/01/22)

Avis 100 % réels, preuves à l’appui

Ridan

Mille mercis (02/01/22)

Avis 100 % réels, preuves à l’appui

Claudine T.

Merci infiniment (15/12/21)

Avis 100 % réels, preuves à l’appui

Laurent G

très bien très réactif et rapide (13/12/21)

Avis 100 % réels, preuves à l’appui

Mounir B.

Merci à vous pour votre gentillesse et professionnalisme (09/12/21)

Avis 100 % réels, preuves à l’appui

Amradouch

Génial super parfait et merci pour les réponses (09/12/21)

Avis 100 % réels, preuves à l’appui

Mohamed S.

Très bien parfait merci (03/12/21)

Avis 100 % réels, preuves à l’appui

CED

Parfait merci beaucoup (01/12/21)

Avis 100 % réels, preuves à l’appui

GC

Parfait, bon boulot (30/11/21)

Avis 100 % réels, preuves à l’appui

M. Sassi

Ok parfait (29/11/21)

Avis 100 % réels, preuves à l’appui

Sami l.

Réponses bien claires, merci (29/11/21)

Avis 100 % réels, preuves à l’appui

D. Emeriau

Je vous remercie pour vos réponses (29/11/21)

Avis 100 % réels, preuves à l’appui

M. COULON

Impeccable merci (19/11/21)

Avis 100 % réels, preuves à l’appui

Denis B .

J'ai bien ouvert le compte bancaire et tout va bien (26/11/21)

Avis 100 % réels, preuves à l’appui

José M.

Merci de tout ce que vous avez fait pour moi (25/11/21)

Avis 100 % réels, preuves à l’appui

Guillaume C.

Super.... Vous êtes réactifs vous avez un bon service (24/11/21)

Avis 100 % réels, preuves à l’appui

MICHEL D.

J'ai bien réceptionné tous vos documents et je vous en remercie bien. Mon avis sur votre prestation est que vous êtes au top, et , comme je vous l'ai dit par téléphone la semaine dernière, je vous remercie encore pour votre rapidité et votre efficacité et vos bons conseils. Je suis vraiment ravi d'avoir fait appel à vos services, (23/11/21)

Avis 100 % réels, preuves à l’appui

Gilles D.

Merci de votre efficacité. Vous avez fait plus vite que prévu. 20/11/21

Avis 100 % réels, preuves à l’appui

Dominique M.

Merci beaucoup pour votre rapidité. C'est parfait, encore bravo pour votre efficacité. (18/11/21)

Avis 100 % réels, preuves à l’appui

Anthony Z.

Le top. Très efficace. Je vais en parler à mes amis. (17/11/21)

Avis 100 % réels, preuves à l’appui

Béatrice D.

Merci de votre patience (12/11/21)

Avis 100 % réels, preuves à l’appui

Jean B

Merci pour votre efficacité (12/11/21)

Avis 100 % réels, preuves à l’appui

Hugo C

Parfait merci beaucoup (08/11/21)

Avis 100 % réels, preuves à l’appui

Samuel C.

Travail respectant les délais. (05/11/21)

Avis 100 % réels, preuves à l’appui

J. MARTINS

Merci beaucoup de votre aide, service rapide. (04/11/21)

Avis 100 % réels, preuves à l’appui

El Debs C.

Tout est nickel, je vous remercie. Excellent service, rapide et efficace. (03/11/21)

Avis 100 % réels, preuves à l’appui

Zitouni A.

Merci de votre professionnalisme (02/11/21)

Avis 100 % réels, preuves à l’appui

Gilbert F.

Prestation parfaite. Merci pour votre soutien. (02/11/21)

Avis 100 % réels, preuves à l’appui

Christian ED

Parfait, top merci (02/11/21)

Avis 100 % réels, preuves à l’appui

Christian

Merci beaucoup vous êtes super (30/10/21)

Avis 100 % réels, preuves à l’appui

David S

Très bien parfait (28/10/21)

Avis 100 % réels, preuves à l’appui

SH

Très bonne prestation. (23/10/21)

Avis 100 % réels, preuves à l’appui

Arnaud R

Je suis très satisfait du service (13/10/21)

Avis 100 % réels, preuves à l’appui

Laurent G

Je vous remercie pour votre réactivité. Je suis très satisfait de vos prestations (13/10/21)

Avis 100 % réels, preuves à l’appui

Patrick W

Ça me convient parfaitement (11/10/21)

Avis 100 % réels, preuves à l’appui

CB

Merci pour votre retour concernant l'introduction ouverture de compte (05/10/21)

Avis 100 % réels, preuves à l’appui

GO

Je suis satisfait de la configuration de la société. Je penses que vous ne pouviez pas faire mieux. Merci encore! (05/10/21)

Avis 100 % réels, preuves à l’appui

Christophe A

Nous vous remercions pour votre célérité à avoir produit la modification souhaitée; notre satisfaction est de 100%. (28/09/21)

Avis 100 % réels, preuves à l’appui

BENTAÏEB

Merci à vous, très bon interlocuteur, agréable et réactif. (24/09/21)

Avis 100 % réels, preuves à l’appui

Anaelle J.

...Parfait... Merci beaucoup... Procédé fluide et efficace...Très bonne communication (23/09/21)

Avis 100 % réels, preuves à l’appui

Rachid EM

Je ne peux que remercier votre entité pour son sérieux et son savoir-faire, grâce à vos compétences (16/09/21)

Avis 100 % réels, preuves à l’appui

GM

Je suis content de votre travail (13/09/21)

Avis 100 % réels, preuves à l’appui

Alexis

Au top (09/09/21)

Avis 100 % réels, preuves à l’appui

Phil

Prestation de qualité et vraiment très rapide. Bravo 🙂 (09/09/21)

Avis 100 % réels, preuves à l’appui

Sébastien H.

Je suis très content, surtout ce qui est important c'est le relationnel avec votre société car dans ce projet on fait confiance. Et votre système Internet et très bien et surtout rapide (07/09/21)

Avis 100 % réels, preuves à l’appui

Jérôme

Très bon service (06/09/21)

Avis 100 % réels, preuves à l’appui

Jeremie L

Totale satisfaction des prestations de votre société, elle se distingue par son sérieux. Merci (27/08/21)

Avis 100 % réels, preuves à l’appui

Nourdine B.

Bonjour J'ai contacté cette société plusieurs fois et j'ai été satisfait à chaque fois de leur suivi à mon égard et de leur réactivité pour leurs réponses puis de leur prise en charge de ma commande. Je les remercie du soutien qu'ils m'ont apporté. (22/08/21)

Avis 100 % réels, preuves à l’appui

Raul JPP

Très satisfait de la prestation. Surtout j'ai toujours reçu un feed-back des questions posées. Merci. (21/08/21)

Avis 100 % réels, preuves à l’appui

Laurent C

« J’ai aimé notre premier échange et l’accompagnement que nous avons eu ensemble tout au long du projet. Une écoute et une sympathie très appréciable. Une rapidité d’exécution, un niveau de compétence bien au dessus du marché. Merci beaucoup pour votre soutien et votre accompagnement dans ce projet. (28/07/21 - 17h13) »

Avis 100 % réels, preuves à l’appui

Dominique G.

« Prestation rapide et efficace (20 juillet 2021, 08h44) »

Avis 100 % réels, preuves à l’appui

Patrick D.

« réussite de la création de ma société - immatriculation de la société dans un délai de 48 h ouvrés comme indiqué sur votre site. Bravo ! (19 juil. 2021 23h43 et 20 juil. 2021 15h06) »

Avis 100 % réels, preuves à l’appui

Sébastien H.

« Parfait. Très bien, rapide. Je suis très content. (16/07/21 - 17h36) »

Avis 100 % réels, preuves à l’appui

Rangel M.

« Je conseille vivement cette équipe à tous ceux qui veulent un service rapide et efficace. (29/06/21 - 17h37) »

Avis 100 % réels, preuves à l’appui

Carlos B.

« Service efficace, dans les délais. Merci. (24/06/21 - 12h37) »

Avis 100 % réels, preuves à l’appui

Mustapha A.

« Tout se passe bien en vous remerciant pour votre service (24/06/21 16:47) »

Avis 100 % réels, preuves à l’appui

Jacques L.

« Très satisfait de votre excellent service ainsi qu'à votre patience à avoir pris le temps de répondre à toutes mes questions.! (21/06/21 - 09h49) »

Avis 100 % réels, preuves à l’appui

Marco B.

« L’équipe est à l’écoute et patiente, je suis ravis du service Merci (15 juin 2021, 10:38) »

Avis 100 % réels, preuves à l’appui

Rezki A.

« Nickel (09/06/21 - ) »

Avis 100 % réels, preuves à l’appui

Anthony V.

« Merci pour votre temps et vos réponses, c’est vraiment très apprécié. Excellent service et support ! Le service relation client répond rapidement. Je suis satisfait des services proposés par service-societe.com. Merci encore une fois pour votre grand travail ! (08/06/21 - 21h14) »

Avis 100 % réels, preuves à l’appui

Loïc O.

« Merci encore pour votre rapidité c’est vraiment un service express!!!!!!!! (07/06/21 - 14h48) »

Avis 100 % réels, preuves à l’appui

Adlène G.

« Je remercie infiniment toute l'équipe qui était à l’écoute chaque fois avec ses très bons conseils, Pour ma part service-societe.com était très réactive et très sérieuse vu que ma société est créée en moins de 48h. (01/06/21 - 15h39) »

Avis 100 % réels, preuves à l’appui

Ahmed B.

« Vous êtes efficace (25 mai 2021, 22h59) »

Avis 100 % réels, preuves à l’appui

Hayman L.

« La prestation est très satisfaisante, le délai de création de la société est plus que respecté. Je suis très satisfait de votre service, merci (25 mai 21) »

Avis 100 % réels, preuves à l’appui

Gilles D.

« Je suis complètement satisfait (24/05/21 - 20h33) »

Avis 100 % réels, preuves à l’appui

Abdel R.

« Un grand merci, je recommande vivement, à l’écoute, rapide et avec beaucoup de professionnalisme, service-societe.com a répondu à mes attentes, et je souhaite recommencer l’expérience pour d’autres projets. (22/05/21 - 22h39) »

Avis 100 % réels, preuves à l’appui

ZIYA K.

« super merci compétence et rapidité (08/02/21 : 22h15) »

Avis 100 % réels, preuves à l’appui

François C.